Pre Money Valuation

Pre-money valuation is the agreed value of a company immediately before it receives a new round of external funding. The relationship between pre-money valuation and investment size determines two critical outcomes: the price per new share issued to investors, and the percentage of the company those investors will own after the round closes. A company with a $10 million pre-money valuation that raises $2 million will have a $12 million post-money valuation, with the new investors owning 16.7% ($2M ÷ $12M) of the fully diluted company.1 Pre-money valuations are negotiated, not calculated — they represent a point of agreement between founders and investors about the company's current worth, incorporating market comparables, traction, growth rate, and the investor's target ownership.3

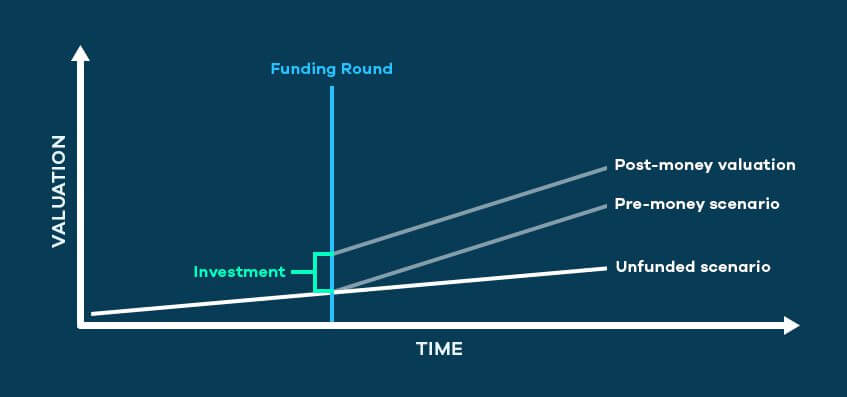

The Core Calculation

The mathematical relationship between pre-money valuation, post-money valuation, and investor ownership is fixed once the investment amount is agreed upon. Post-money valuation equals pre-money valuation plus the investment amount; investor ownership percentage equals investment amount divided by post-money valuation.7 For a concrete example: if a company raises $5 million at a $20 million pre-money valuation, the post-money valuation is $25 million, and the investor owns 20% of the fully diluted company. The price per share is derived by dividing the pre-money valuation by the total fully diluted share count before the round; if there are 10 million fully diluted shares outstanding, the price per share is $2.00, and the $5 million investment purchases 2.5 million new shares.2

The framing of valuation as "pre-money" versus "post-money" has significant practical consequences for founders who don't model both. An investor who says "we want to invest $5 million at a $25 million valuation" is almost certainly quoting a post-money figure — meaning the pre-money is $20 million and they're targeting 20% ownership. A founder who hears "$25 million valuation" and assumes it's pre-money would be giving the investor only 16.7% ($5M ÷ $30M post-money), a meaningful difference.5 This framing confusion is more common at seed stage, where SAFE instruments delayed the negotiation of explicit pre-money figures — Y Combinator's post-money SAFE, introduced in 2018, caps investor ownership at a defined post-money percentage and eliminates this ambiguity.3

How VCs Arrive at Valuations

Early-stage venture capital valuation is not a precise science. Most Series A investors apply a target ownership model: a fund that needs to own at least 15–20% of a company to justify the time and board seat commitment will work backward from that ownership target to determine the maximum pre-money valuation they're willing to accept for a given check size.4 A fund writing a $5 million Series A check and targeting 20% ownership will accept at most a $20 million pre-money valuation. If the founder insists on $30 million pre-money, the fund either increases the check to $7.5 million or passes.

The Venture Capital Method, formalized by Harvard Business School professor William Sahlman, structures this backward calculation explicitly. The investor forecasts an exit value — typically by applying a revenue multiple from comparable public companies to the startup's projected revenue in 5–7 years — then discounts that exit value by a required rate of return (often 10x–30x for seed, 5x–10x for Series A) to derive acceptable post-money valuation today.6 For example: a startup projected to generate $50 million in revenue in year 5, in a sector where comparable public companies trade at 5x revenue, implies a $250 million exit value. An investor requiring a 10x return would pay at most $25 million post-money today, implying a pre-money valuation of $20 million for a $5 million investment.8

Comparable company analysis (CCA) grounds valuations in market reality by benchmarking against companies at similar stages in similar sectors that have recently raised or been acquired.1 In practice, VC valuation incorporates both the comparable framework and the fund's ownership requirements, with the final figure settled in negotiation. Andreessen Horowitz has published that typical Series A valuations in software were $10–30 million pre-money in 2012, $30–80 million in 2018, and $40–150 million in 2021 during the peak funding environment, with the range compressing back toward $20–60 million in 2023.4

Real Deal Examples

Facebook raised a $500,000 seed round from Peter Thiel in June 2004 at a $4.9 million pre-money valuation, giving Thiel approximately 10.2% ownership at a post-money valuation of $5.4 million — a stake worth approximately $1 billion at Facebook's 2012 IPO.2 Airbnb raised a $600,000 seed round in early 2009 from Sequoia Capital and others at a pre-money valuation of roughly $2.4 million; the company was valued at $10 billion by 2014, a roughly 4,000x increase in enterprise value from the seed pre-money figure.3

At Series A, the median pre-money valuation in the US was approximately $22 million in 2020 and climbed to $42 million by 2021, according to PitchBook data, before declining to approximately $28 million in 2023.4 Series B pre-money valuations in 2022 median around $120–150 million in software. These figures vary substantially by sector: biotech Series A valuations routinely exceed $50 million despite no revenue, while consumer apps face more pressure to show growth metrics.2

Valuation Methods for Pre-Revenue Companies

When a company has no revenue, traditional DCF and CCA approaches are difficult to apply directly. The Berkus Method, developed by angel investor Dave Berkus, assigns up to $500,000 in value to each of five factors: sound idea, prototype, quality management team, strategic relationships, and product rollout or sales.6 This gives a maximum pre-money valuation of $2.5 million for a pre-revenue company, a ceiling that reflects typical seed-stage angel investment norms of the early 2000s. The Risk Factor Summation Method assigns a baseline value of $1–2.5 million to a pre-revenue startup and then adjusts that baseline up or down based on 12 risk factors including management, stage, manufacturing, sales, and litigation risk.8

In practice, most pre-revenue seed valuations in the 2020s are set by market convention more than formal models. Y Combinator alumni companies exiting YC Demo Day in 2023 commonly raised at post-money valuations of $12–20 million (implying pre-money of $8–16 million for a $2–4 million raise), a figure driven by YC's brand, competitive investor interest at Demo Day, and the prevailing market for YC-caliber deals.3 The existence of a competing term sheet from another investor is the single most powerful lever for increasing a pre-money valuation, regardless of what any formal model suggests.4