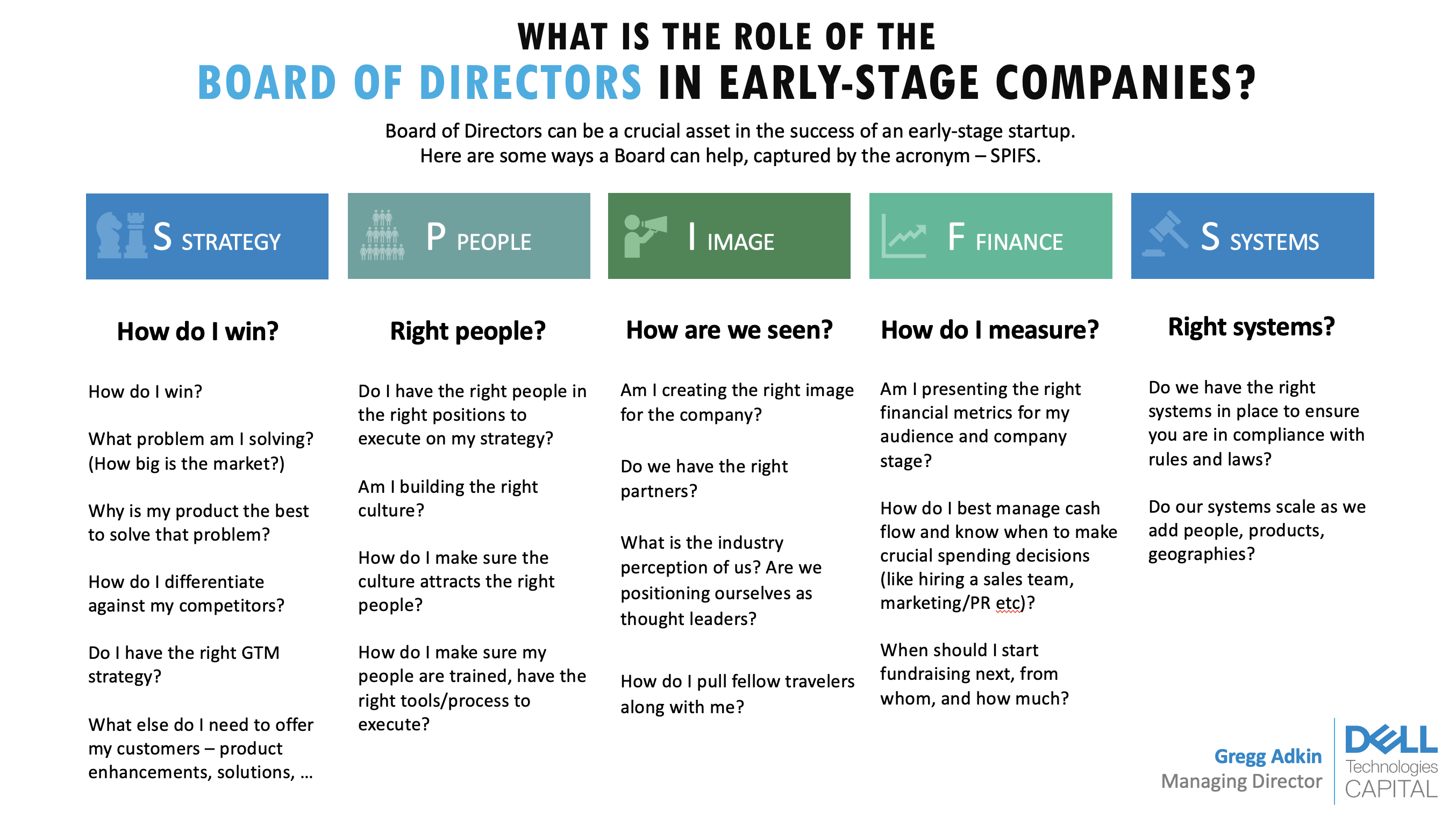

Board Seat

A board seat in venture capital is a directorship on a portfolio company's board of directors, giving the holder the legal right to vote on major company decisions and imposing fiduciary duties to act in the interest of all shareholders. Lead investors typically negotiate one board seat per funding round starting at Series A; at seed stage, board seats are less common and most investors accept observer rights instead.2 A typical Series A board has 5 members: 2 founders, 1 VC director, 1 independent director, and 1 optional seat that may go to a second investor or second independent.3 Board composition is one of the most consequential provisions in a term sheet because it determines who controls the company in the event of disagreements over strategy, executive changes, or liquidity events.

When VCs Demand Board Seats

Venture capital firms that lead a funding round — writing the largest single check and negotiating the term sheet — almost always take a board seat as part of the investment terms. The logic is straightforward: a fund investing $5–10 million into a company needs governance access to protect that investment, and board membership provides the oversight mechanism.3 Non-lead investors, those participating but not setting terms, typically receive observer rights at most.

At seed stage (pre-Series A), board seats are unusual because the company is not yet institutionally funded and the investor relationships are often with angels or small funds. Y Combinator explicitly advises its companies not to grant board seats to seed investors, and most YC graduates maintain a 2-person founder-controlled board (or no formal board at all) through their seed rounds.2 The transition to a formal board typically occurs at Series A, where the lead investor — often a firm like Sequoia Capital, Andreessen Horowitz, or Benchmark — receives one seat as a standard condition of the investment. By Series B, most companies have boards of 5 members. As companies raise Series C and later rounds, board size sometimes grows to 7–9 members, though governance experts recommend capping at 7 to maintain efficiency.1

Fiduciary Duties and the Dual Fiduciary Problem

Board directors — including VC-appointed directors — owe fiduciary duties of loyalty and care to the corporation and its stockholders under Delaware law, the jurisdiction that governs most US-incorporated startups.1 The duty of loyalty requires directors to act in the best interests of the company as a whole, placing company interests above personal financial interests. The duty of care requires directors to act on an informed basis, having reviewed materials and participated meaningfully in deliberations before voting.

VC-appointed directors are "dual fiduciaries," as described by Wilson Sonsini Goodrich & Rosati partners Steven Bochner and Amy Simmerman in a Delaware Journal of Corporate Law article: they owe duties to the company's common stockholders (primarily founders and employees) while simultaneously being employed by, and owing duties to, the fund and its limited partners.1 This creates structural conflict when the interests of preferred stockholders (investors) diverge from common stockholders (founders and employees). Down-round financings with punitive anti-dilution provisions, recapitalizations that reduce common equity, and acquisitions at prices that return money to preferred holders while wiping out common — all are transactions where VC directors face a direct conflict between their fund duties and their board duties.

Delaware courts have addressed these conflicts in a series of cases. In re Trados Inc. Shareholder Litigation (2013), the Delaware Court of Chancery found that board directors had breached their fiduciary duties by approving a management incentive plan and merger transaction structured to benefit preferred holders while leaving common stockholders with nothing, despite the common stockholders being the primary beneficiaries of the directors' fiduciary duties.1 The Trados decision established that VC board members who are financially conflicted — holding preferred stock while voting on transactions that allocate proceeds between preferred and common — must ensure an independent committee process or face enhanced scrutiny that the business judgment rule will not protect them.

Observer Rights vs. Voting Rights

Board observers attend board meetings, receive board materials, and may participate in discussions, but have no vote on any decision and owe no fiduciary duty.4 Investors at seed stage typically receive observer rights; the seed investor who wrote a $500,000 check into a company that later raises a $10 million Series A will commonly see their board seat request denied and accept observer status instead.2 Observers can be excluded from sensitive discussions at the board's discretion — the board may ask observers to leave the room when discussing CEO performance reviews, potential acquisitions, or any matter in which the observer has a conflict of interest.

The practical value of observer seats is meaningful: observers receive the same financial reports, board decks, and strategic information as directors, enabling them to monitor their investment. The 2025 Harvard Law School Corporate Governance article on board observers noted the increased use of observer rights as investor leverage has grown, particularly in competitive seed rounds where investors unable to negotiate a board seat seek observer access as an information protection mechanism.4 However, observers gain no legal protection from the duty of care, meaning their attendance does not constitute informed oversight in any legally meaningful sense.

Information rights — the right to receive periodic financial statements and other company information — are distinct from observer rights. A founder can grant information rights without granting board access; the combination of information rights plus observer rights is the standard package for seed investors who invest more than $500,000.7

Governance Controversies

The governance structure of VC-backed companies has produced high-profile controversies when board composition allowed investors to override founder preferences. Travis Kalanick's removal as Uber CEO in June 2017 was executed by a board vote after five investors — including Benchmark, which held board seats — sent a letter demanding his resignation.1 Benchmark's Eric Vishria, as a board member, was among the signatories; the decision was legally unimpeachable because investors had accumulated sufficient board and shareholder voting rights to compel the outcome, but it established that VC board seats can translate into CEO removal even against a founder's wishes when the investor coalition is large enough.

Adam Neumann's removal as WeWork CEO in September 2019 followed a similar dynamic: SoftBank, as the largest preferred stockholder with board representation, led a process that forced Neumann's resignation amid the failed IPO. The WeWork board structure — which included multiple VC-appointed directors and gave Neumann's shares supervoting rights that he ultimately couldn't use effectively after the IPO collapsed — illustrated how board seat accumulation by investors over multiple rounds creates governance structures that can shift power rapidly when a liquidity event fails.5

Founders seeking to protect their governance position commonly negotiate for supervoting common shares (Class B shares with 10 votes per share versus 1 vote per share for Class A) in their certificate of incorporation. Google (1998), Facebook (2004), Snap (2017), and Lyft (2019) all went public with dual-class structures that preserved founder voting control regardless of economic dilution.1 At the private company stage, founders negotiate to maintain board majority by filling the independent director seats with individuals they choose or by ensuring that the combined investor seat count never exceeds the combined founder and independent seat count until a liquidity event.2