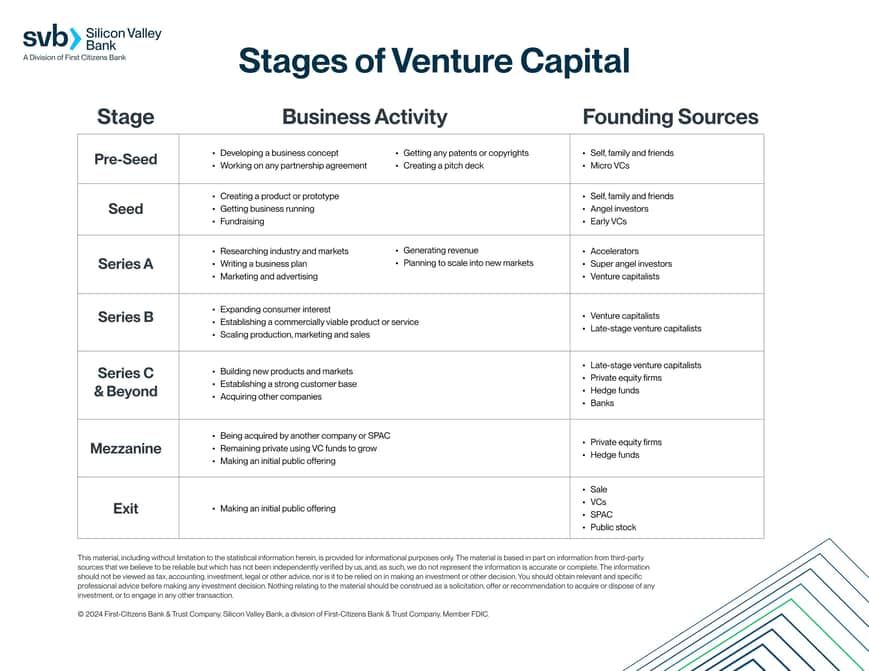

Series C

A Series C is the third major institutional equity round a startup raises, typically deployed to scale operations into new markets, fund acquisitions, or build toward an IPO. Series C valuations range from $100M to $500M or higher, with median pre-money valuations in the $300–$400M range based on PitchBook data.6 Only approximately 1% of startups that begin raising venture capital reach Series C.6 Carta reported $3.5 billion in total Series C funding among companies on its platform in Q4 2024 alone, with activity at its lowest point in late 2023 before recovering through 2024.1

Structure and investor composition

A Series C is structured as a priced preferred stock round, but the composition of investors changes significantly from earlier rounds. While venture capital firms may lead or participate, Series C rounds routinely include hedge funds, mutual funds (such as Fidelity and T. Rowe Price), private equity groups, and investment banks that do not participate in Series A or Series B transactions.2 These late-stage institutional investors accept lower expected multiples in exchange for lower risk: the company has an established customer base, known revenue trajectory, and a clearer path to liquidity.

The typical dilution at Series C is 10–20%, lower than at Series B, because companies at this stage have more negotiating leverage: they generate substantial revenue, have multiple investors competing to participate, and can credibly project an IPO timeline.7 The average Series C round raises approximately $50M, though outlier rounds frequently exceed $100M. Ant Group raised a $14B Series C in 2018 — the largest single Series C in history — and CoreWeave raised a $1.1B Series C in 2024 ahead of its IPO.2

Governance structures at Series C often involve a formal audit committee, outside legal counsel, and quarterly reporting standards that approach public company requirements. Many Series C term sheets include IPO ratchets — provisions that give investors additional shares if the IPO price falls below a threshold — and drag-along rights that allow a majority of preferred shareholders to compel a sale. Companies with multiple rounds of preferred stock face complex negotiations around liquidation preference stacks, which determine how proceeds are distributed in a sale below the last-round valuation.2

What investors require

Series C investors evaluate a company on hard financial metrics. B2B SaaS companies with revenues between $10M and $20M ARR, strong gross margins, and a demonstrated path to $100M ARR are the typical Series C profile.9 Gross margin, customer concentration, net revenue retention, and sales efficiency (measured as the ratio of revenue growth to sales spend) are the primary quantitative inputs. A company spending $1 to generate $1 of new ARR faces harder terms than one spending $0.50.

Investors at this stage assess the management team's ability to run a public company. The CFO, general counsel, and VP Sales roles are scrutinized, and Series C investors often require that a company have completed a Big Four audit for at least one fiscal year. Board composition matters: investors look for independent directors with public market experience. The combination of financial and operational readiness distinguishes a Series C company from one that merely has sufficient revenue for a large round.9

The time between Series B and Series C hit decade highs in 2024, surpassing two years according to the Q4 2024 PitchBook-NVCA Venture Monitor.5 Companies that raised Series B rounds at inflated 2021 valuations and failed to grow into those valuations found the Series C market effectively closed to them — unable to raise at a higher valuation and unwilling to accept a down round, many pursued bridge financing or M&A rather than a priced Series C.

Notable examples

Stripe raised an $80M Series C in January 2014, led by Sequoia Capital with participation from Founders Fund and Khosla Ventures, at a $1.75B valuation.3 The round funded Stripe's international expansion into Europe and Asia. Stripe then raised a Series D at $3.5B just 11 months later, in December 2014, reflecting how quickly its payments volume had scaled.3

Airbnb raised a $475M Series C in August 2014 led by Sequoia Capital and Andreessen Horowitz, at a reported valuation of approximately $10B.4 The round reflected Airbnb's presence across 190 countries with over 600,000 listings and was one of the largest rounds ever raised by a consumer marketplace at the time. Snowflake raised a $45M Series C in June 2015, led by Altimeter Capital, as the company came out of beta.8 Snowflake continued to raise additional rounds before its September 2020 IPO, which priced at $120 per share and valued the company at $33.2B — the largest software IPO in history at the time.

Magic Leap raised a $793.5M Series C in 2016 led by Alibaba Group, and Gorillas raised a $1.0B Series C in 2021 at peak market conditions.2 The largest Series C rounds are concentrated in sectors with winner-take-most dynamics — payments, cloud infrastructure, autonomous vehicles, and AI — where investors are willing to price in category-leadership premiums at late stage.

Exit paths from Series C

The three primary exit paths for Series C companies are IPO, strategic acquisition, or continued private financing through Series D and beyond. The IPO path requires 2–3 consecutive years of audited financials, demonstrated public-market-comparable revenue multiples, and investment banker relationships established 12–18 months before filing. Venture capital firms that led earlier rounds typically introduce the company to long-only institutional investors well before a planned offering.9

Strategic acquisitions at the Series C stage are common in sectors where large technology companies, financial institutions, or healthcare conglomerates value the startup's technology or customer base above public market multiples. The NVCA's 2024 data showed that exit activity remained constrained, with large exits above $500M representing only 3.6% of completed exits but accounting for 78.9% of total exit value.5 This concentration of returns in a small number of large outcomes shapes how Series C investors underwrite their expected return — they price most investments assuming the company reaches IPO or strategic acquisition above $1B, not a sub-$500M acqui-hire.