Pro-Rata Rights

Pro-rata rights (sometimes written pro rata) are a contractual guarantee that gives an investor the right — but not the obligation — to participate in a company's subsequent funding rounds in an amount sufficient to maintain their existing ownership percentage.1 The rights are negotiated in a term sheet or a separate side letter and attach to the investor, not the shares.2 Nearly all institutional venture capital investors seek pro-rata rights because they allow fund managers to increase their position in portfolio companies that outperform — the strategy known as "doubling down on winners."1

Mechanics and Calculation

Pro-rata rights are calculated relative to the investor's current ownership at the time the new round closes. If an investor owns 5% of a company before a Series A, their pro-rata allocation is the number of new Series A shares required to keep their ownership at 5% post-close.1

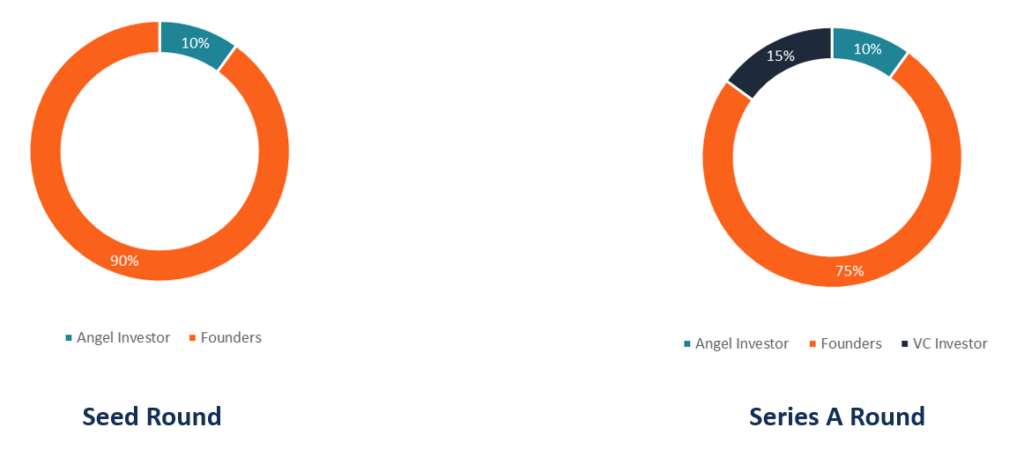

A worked example: FastCapital VC invests $100K in Widgets Inc.'s seed round at a $3M pre-money valuation, receiving 50,000 shares out of 2,000,000 total shares — a 2.5% ownership stake. Widgets later raises a Series A at an $8M pre-money valuation with 2,000,000 shares already outstanding, issuing 500,000 new shares at $4.00 each. To maintain 2.5% post-Series A (2.5% × 2,500,000 = 62,500 shares), FastCapital must buy 12,500 new shares at $4.00 = $50,000. If FastCapital declines to exercise, its ownership falls from 2.5% to 2.0%.1

Pro-rata rights can be structured on three bases. The percentage basis is by far the most common — investors maintain their exact ownership percentage by investing whatever dollar amount that requires in each subsequent round.2 The dollar-for-dollar basis allows investors to invest up to the same dollar amount they invested in their first round, regardless of percentage impact — a $250K seed investor may reinvest up to $250K in the Series A. The fixed-sum basis specifies a pre-agreed dollar amount the investor may invest in each future round, decoupled entirely from their original investment.2 Dollar-for-dollar and fixed-sum bases can produce "super pro rata" rights when the specified amount exceeds what percentage maintenance would require.

Super Pro Rata and Its Risks

Super pro rata rights grant an investor the ability to buy a larger ownership stake in a subsequent round than they currently hold — for example, the right to invest $2M in a Series A when percentage maintenance would only require $500K.2 They can emerge explicitly (a term granting 2x the investor's current ownership allocation) or implicitly (dollar-for-dollar pro rata for an investor whose percentage has grown substantially).

Super pro rata rights create friction with new lead investors. A typical Series A firm targets 15–20% ownership in a company. If an existing angel holds super pro rata rights that consume 15% of the round's available allocation, the new lead investor either reduces their target ownership or the founders must sell a larger total percentage than intended.2 This dynamic can deter lead investors from engaging with a company at all — the signal that an inside investor has aggressive super pro rata rights sometimes reads as a vote of no-confidence from that investor if they later choose not to exercise them.2

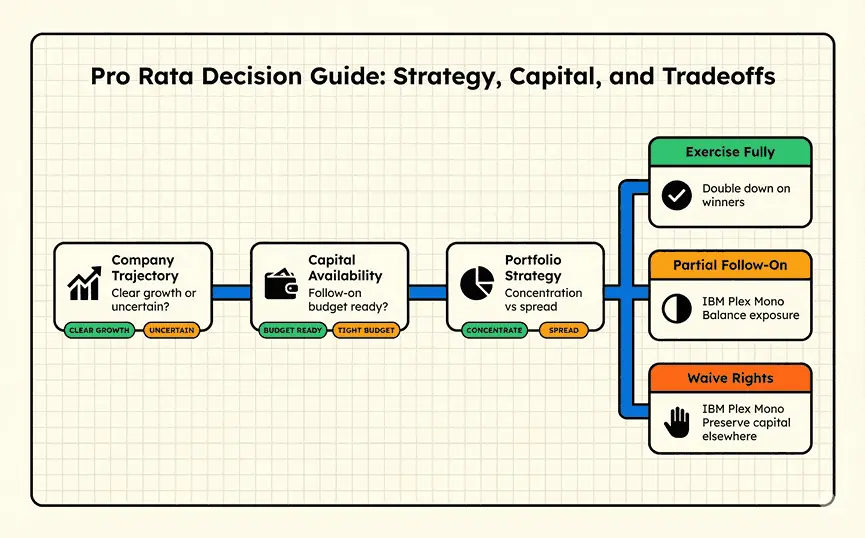

Investor Strategy: When to Exercise

Exercising pro-rata rights requires reserved capital. Venture funds that deploy all capital in initial investments cannot exercise pro rata even if they want to. Fund managers routinely disclose to their limited partners whether they maintain reserves for follow-on investments and at what ratio — common ratios are 1:1 (equal capital reserved for follow-on as for initial investment) or 2:1.3

AngelList data on seed-stage portfolios shows that always following on generates a higher mean return (TVPI), while never following on generates a higher median return.1 This reflects the power-law distribution of venture returns: broadly indexing across many seed investments captures outliers more reliably than concentrating reserves in follow-on investments that may crowd out new early-stage bets. Selectively following on did not demonstrably outperform either extreme in AngelList's 100,000-simulation study.1

First Round Capital's 5,000x return on Uber at IPO in 2019 is the canonical example of pro-rata value: investors who held and exercised pro rata in early Series B and later rounds locked in meaningful ownership of a company that became one of the most valuable in history.1 The asymmetry of venture outcomes — where a single investment can return the entire fund — makes preserving the option to follow-on in breakout companies one of the highest-value rights a seed investor can hold.

Granting Strategy for Founders

Founders must decide which investors receive pro-rata rights and at what threshold. The most common approach is a major investor threshold: only investors who commit above a specified minimum (e.g., $500K) receive pro-rata rights.2 Angel investors typically fall below the threshold and resent being excluded; institutional VCs demand inclusion. Setting the threshold too low creates a large group of investors who must all be consulted and accommodated in every subsequent round.2

Pro-rata rights survive into future rounds once granted. A founder who gives pro-rata rights to an angel in the seed round must accommodate that angel's allocation in every future round unless the rights are waived. In a competitive Series A where a lead investor wants to own 20% and every existing angel exercises pro rata, the total dilution to founders can substantially exceed what the headline round size implies.5

Some founders use pro-rata rights as a negotiating lever — offering them to investors who bring strategic value (customer introductions, hiring pipelines, board-level expertise) in exchange for lower entry valuations or more favorable terms.6 The value of pro-rata rights to an investor increases dramatically as the company performs: an investor who bought 2.5% of a seed-stage startup for $100K has an extremely valuable pro-rata right if the company later raises at a $500M valuation, as maintaining that 2.5% would now cost $12.5M but grant access to an allocation that outside investors cannot obtain at any price.7