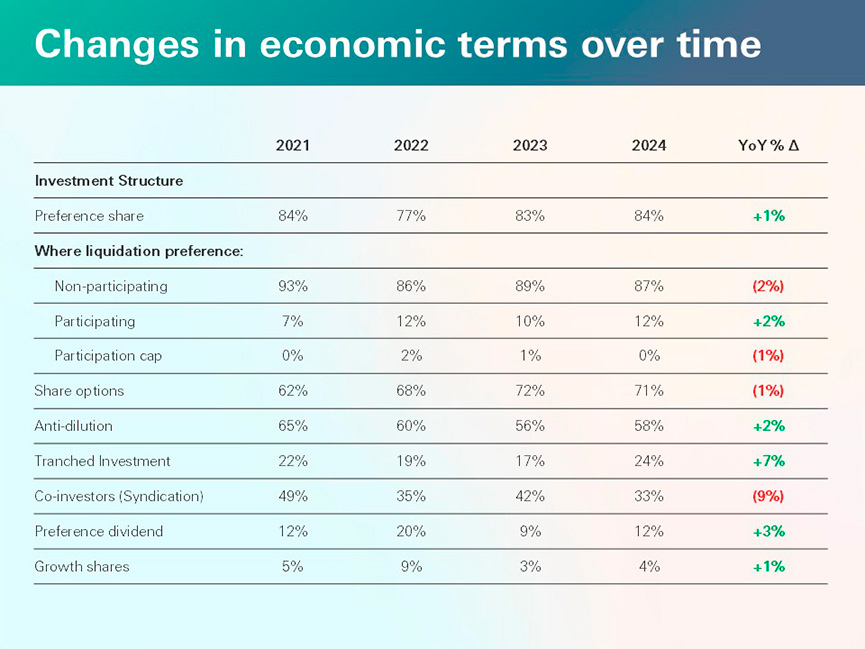

Liquidation Preference

A liquidation preference is a negotiated clause in preferred stock that entitles investors to receive a specified multiple of their invested capital before common stockholders receive any proceeds in a liquidation event — including a sale, merger, or wind-down.1 The preference is the defining economic right that makes preferred stock "preferred," and Cooley GO identifies it as the second most important business issue in any term sheet after valuation.2 A 1x non-participating liquidation preference is the current NVCA standard and the most founder-friendly structure an investor with downside-protection needs will accept.3

Mechanics

The liquidation preference sits at the top of the distribution waterfall — the ordered sequence in which exit proceeds are paid out across all cap table holders. When a company sells or is otherwise liquidated, preferred stockholders exercise one of two options: take the preference amount (remaining in preferred stock) or convert to common stock and receive their pro-rata share of total proceeds.3 Rational investors choose whichever is higher. In a $100M exit where a Series A investor owns 25% and invested $5M with a 1x preference, they will convert to common and take $25M rather than their $5M preference. In a $10M exit, they take the $5M preference rather than $2.5M.1

The preference is expressed as a multiple of invested capital. A 1x preference entitles the holder to exactly their investment back before any distribution to common. A 2x preference returns double the investment, and a 3x preference returns triple, before common shareholders see anything. Multiples above 1x are uncommon in competitive fundraising environments — they were prevalent during the dot-com era but became rare after the 2008 financial crisis as founder leverage increased.4 In strong markets, even sophisticated Series A firms typically accept a 1x non-participating preference.

The seniority structure determines the payout order when multiple rounds of preferred stock coexist on the cap table. The three standard structures are: (1) standard (last-in, first-out — most recent round paid before earlier rounds), (2) pari passu (all preferred series share proceeds pro rata to their invested capital simultaneously), and (3) tiered (a hybrid grouping rounds into tiers that pay out pari passu within each tier).1 Series A terms set at a company's first institutional round frequently carry forward into Series B and beyond, meaning a heavy preference negotiated early compounds through subsequent rounds.2

Participation Rights

Participation rights define whether preferred stockholders can "double dip" — collect their preference and then share in remaining proceeds alongside common stockholders. This distinction has more economic impact than the multiple in most ordinary-outcome exits.6

Non-participating preferred (also called straight preferred) requires investors to choose between their preference or common conversion — they cannot take both. An investor who put in $5M with a 1x non-participating preference at a 25% stake in a $50M exit will convert to common and take $12.5M, abandoning the $5M preference. Non-participating is the most founder-friendly structure and represents the NVCA model term.1

Fully participating preferred (participating preferred, or double-dip) entitles investors to receive their full preference first, then participate pro rata alongside common stockholders in all remaining proceeds as if they had converted. An investor with $5M invested, a 1x fully participating preference, and 25% ownership in a $50M exit takes $5M off the top, then receives 25% of the remaining $45M ($11.25M), for a total of $16.25M versus $12.5M under non-participating.1 Cooley GO recommends founders resist fully participating preferred as early-round terms because the structure propagates to every subsequent round.2

Capped participating preferred is a hybrid: the investor participates alongside common until they have received a total aggregate amount of X times their investment (e.g., a 3x cap). Once the cap is reached, the investor may still elect to convert to common entirely and participate without a ceiling — the cap merely limits the double-dip at lower exit values.1 A $1M investment with 1x participating preference and a 3x cap permits a maximum of $3M before converting becomes more favorable.

Preference Stack and Waterfall Modeling

As companies raise multiple rounds, the preference stack grows. Eventbrite's pre-IPO cap table included distinct Series A through Series E preferred tranches, each with independent preference terms and seniority.1 Modeling the waterfall requires tracking, for each round: (1) the preference multiple, (2) the participation type, (3) the seniority tier, and (4) the conversion price — because rounds that stay in preferred change the denominator for remaining rounds.3

The math becomes non-trivial when senior preferred investors convert while junior preferred investors stay in preferred. When a Series A investor converts to common, the remaining Seed investors' ownership percentage in the common pool increases — they owned a smaller slice of a company that now has fewer competing claims. In a $10M exit where Series A (25%) converts but Seed (15%) stays in preferred for a $2M preference, the Seed holders' effective common ownership of the non-preferred pool rises to approximately 20% of the $5M remainder.3

Founders should model three scenarios for every term sheet: a disappointing exit at 1–2x invested capital, a moderate exit at 3–5x, and a strong exit above the total preference stack. Liquidation preferences reduce founder proceeds most severely in the moderate-exit scenario, where the preferences consume a substantial fraction of total proceeds but the company is not valuable enough for everyone to convert to common.4

Negotiation and Founder Implications

The standard market position for a Series A in the U.S. is a 1x non-participating liquidation preference with standard (last-in, first-out) seniority.2 Any deviation — higher multiple, participating preferred, or pari passu seniority that disadvantages newer investors — warrants negotiation. Participating preferred in a small seed round may seem immaterial in dollar terms, but it establishes a precedent that later Series B and later investors will reference when negotiating their own terms.2

Some investors attempt to insert accruing dividends alongside the preference, which effectively raises the preference multiple over time — a $5M investment with 8% accruing dividends carries a preference equivalent to $5.4M after one year and $7.35M after five years, regardless of whether dividends are ever declared.4 Cooley GO identifies accruing dividends as one of the few boilerplate terms worth scrutinizing, unlike non-accruing dividends which are largely ceremonial.2

Pay-to-play provisions occasionally appear alongside liquidation preferences: investors who decline to participate in a down round lose their preference rights and convert to common stock.5 This mechanism forces existing investors to support distressed companies in exchange for retaining their economic protections. The NVCA model documents include an optional pay-to-play provision that founders can use during difficult fundraising environments to align investor incentives with company survival.5