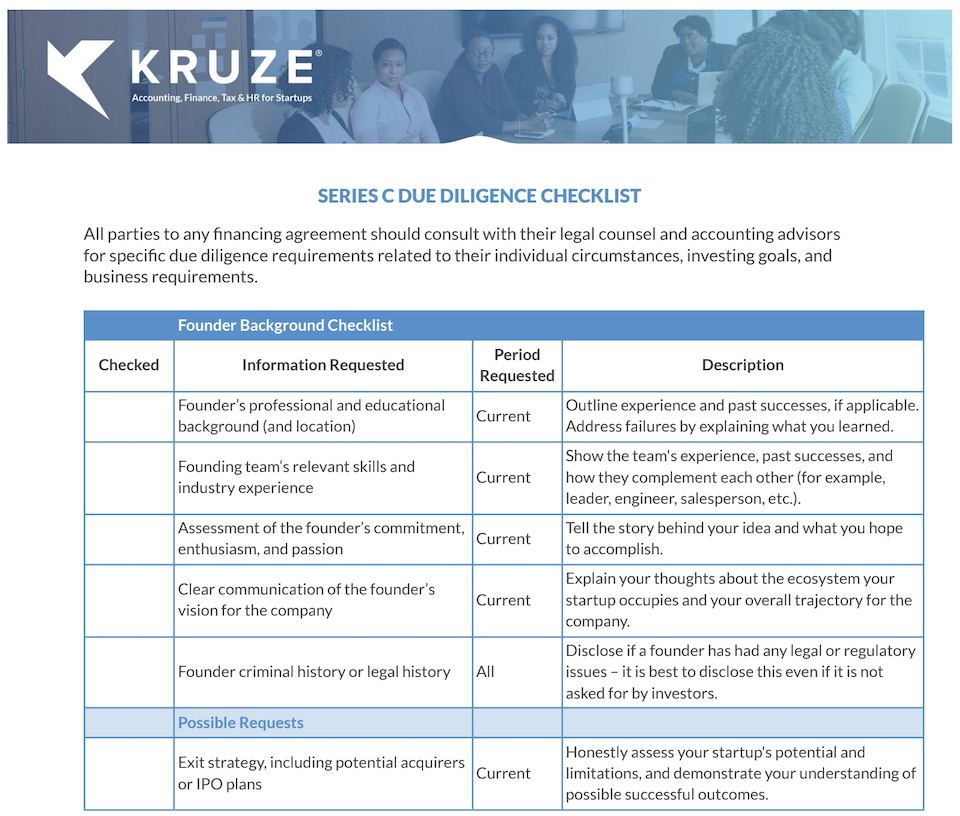

Due Diligence

Due diligence in venture capital is the structured investigation an investor conducts after expressing serious interest in a company and before wiring funds. It typically begins after a term sheet is signed or a verbal agreement reached and spans 2–8 weeks for early-stage deals and 2–4 months for growth-stage rounds where the investment is larger and legal complexity is greater.1 The process covers five workstreams: team assessment, market and competitive analysis, financial review, legal review, and technical or product assessment. Inadequate due diligence is among the most commonly cited causes of failed investments; a 2019 Kauffman Foundation study found that investors who spent more than 20 hours on diligence achieved substantially higher returns than those who spent fewer than 10 hours.3

The Due Diligence Process

The standard VC due diligence process begins with an initial screening phase, during which the investor reviews the pitch deck, financial model, and any existing data room materials to identify obvious disqualifiers before committing significant time.1 Investors commonly refer to this as "top of funnel" diligence — checking for inconsistencies in the pitch narrative, gaps in legal formation documents, or customer concentration issues that might disqualify the deal before deeper analysis. A company that derives more than 40–50% of revenue from a single customer will face this objection immediately.5

If the deal passes initial screening, the investor assembles a diligence team and sends a formal document request list. A typical early-stage document request for a Series A includes: certificate of incorporation and bylaws, all prior financing documents (SAFEs, convertible notes, prior stock purchase agreements), the cap table on a fully diluted basis, 3 years of financial statements (audited if available, management-prepared otherwise), bank statements for the prior 12 months, the current financial model with assumptions, all material customer contracts, key employee offer letters and any non-compete agreements, IP assignment agreements for all founders, pending or threatened litigation disclosures, and any existing board materials or investor updates.2 Growth-stage rounds add audited financials for 2–3 years, third-party market sizing studies, and detailed unit economics documentation.

Customer and reference calls are among the most revealing diligence activities and among the least systematic. Most investors will call 3–10 customers; the best investors call customers the founder did not provide, finding them through LinkedIn, portfolio company networks, or direct outreach. Andreessen Horowitz has described a process in which analysts cold-contact customers from the company's LinkedIn connections to get unscripted feedback, specifically asking: "Why did you buy?", "What would make you cancel?", and "Who else did you consider?"4 Reference calls on founders typically target former colleagues, co-workers from previous companies, and — in markets where it is culturally accepted — former managers and direct reports.

Financial Due Diligence

Financial diligence for a pre-revenue or early-revenue startup focuses on the plausibility of projections and the coherence of the unit economics model rather than historical financial performance. The investor will reconstruct the revenue model from first principles: if the company projects $10 million ARR in year 3 with an average contract value of $50,000, that implies 200 customers — the investor will assess whether the sales team can realistically close 200 enterprise deals.1 Burn rate and runway calculation is validated against bank statements; discrepancies between the financial model's claimed burn rate and actual bank statement outflows are a significant red flag.5

For companies with 12+ months of revenue history, investors analyze gross margin trends, cohort retention (typically presented as net revenue retention or dollar retention), customer acquisition cost by channel, and LTV:CAC ratios. A software company with gross margins below 60% or net revenue retention below 100% will face hard questions in diligence, as both metrics directly affect the terminal value models used to justify the investment.3 Investors at firms like Sequoia Capital and Benchmark will also stress-test the base case model by cutting the assumed growth rate by 50% and checking whether the business survives to the next round on existing capital.4

Legal Due Diligence

Legal diligence, typically performed by outside counsel hired by the investor, reviews every document that could create liability or ownership complications. The most consequential areas are: IP ownership (whether all founders have signed IP assignment agreements, often called PIIAs, vesting all work product into the company), cap table accuracy (whether every prior financing transaction is documented and the share count reconciles), employee agreements (non-competes from prior employers that could prevent founders from working in the company's space), and regulatory compliance (particularly important for fintech, healthtech, and companies handling personal data under GDPR or CCPA).2

Undisclosed litigation is the most common legal red flag and the one most likely to kill a deal in late-stage diligence. Companies that have received a cease-and-desist letter from a competitor, have a former employee with a discrimination or harassment claim, or have regulatory investigations pending must disclose these proactively — discovering them in diligence rather than from the founder creates trust issues that often terminate the process.5 IP disputes with former employers of founding team members — where a prior employer claims the startup's core technology was developed on company time — are the most frequently lethal single legal issue in early-stage diligence.3

Red Flags and Deal Killers

Experienced investors maintain informal mental models of the most common patterns that predict failure. Inconsistencies between the pitch narrative and the data room are the most common category: a founder who claims 200% year-over-year growth in the deck but whose bank statements show 80% growth will lose investor trust immediately.5 Other common red flags include: a cap table with a founder who left in the first year owning more than 10–15% of the company with no buyback agreement (this creates incentive problems and complications in future rounds), customer churn that the company is not actively tracking or has not disclosed, and any hint that the company is shopping a term sheet to manufacture competitive pressure while the deal has not actually been signed.1

The diligence process for founder character is informal but can be decisive. Most institutional VCs will conduct 5–15 reference calls on founding CEOs before closing a deal, asking specifically about integrity, self-awareness, and how the person performs under pressure.4 The collapse of Theranos — in which Elizabeth Holmes concealed fundamental technology failures from investors across multiple due diligence processes — produced lasting changes in how healthcare-focused VCs conduct technical diligence, including more frequent requests for independent expert validation of core technology claims rather than accepting founder presentations.3 Several prominent early Theranos investors later stated that thorough reference calls would have surfaced the fraud years earlier had they been conducted with appropriate rigor.