Anti-Dilution

Anti-dilution protection is a provision in preferred stock that automatically adjusts the conversion ratio of preferred shares into common stock when a company raises new capital at a price lower than the price paid by earlier investors — a "down round."1 The adjustment increases the number of common shares that each preferred share converts to, partially compensating earlier investors for the value lost in the down round.3 Nearly all Series A and later venture financings in the United States include anti-dilution protection in some form, with broad-based weighted average being the standard; full ratchet provisions are rare and widely considered a red flag in term sheet negotiations.4

Why Dilution Matters in Down Rounds

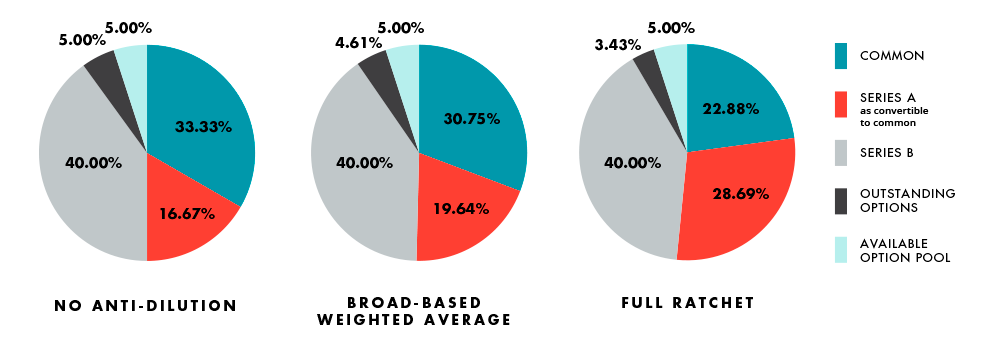

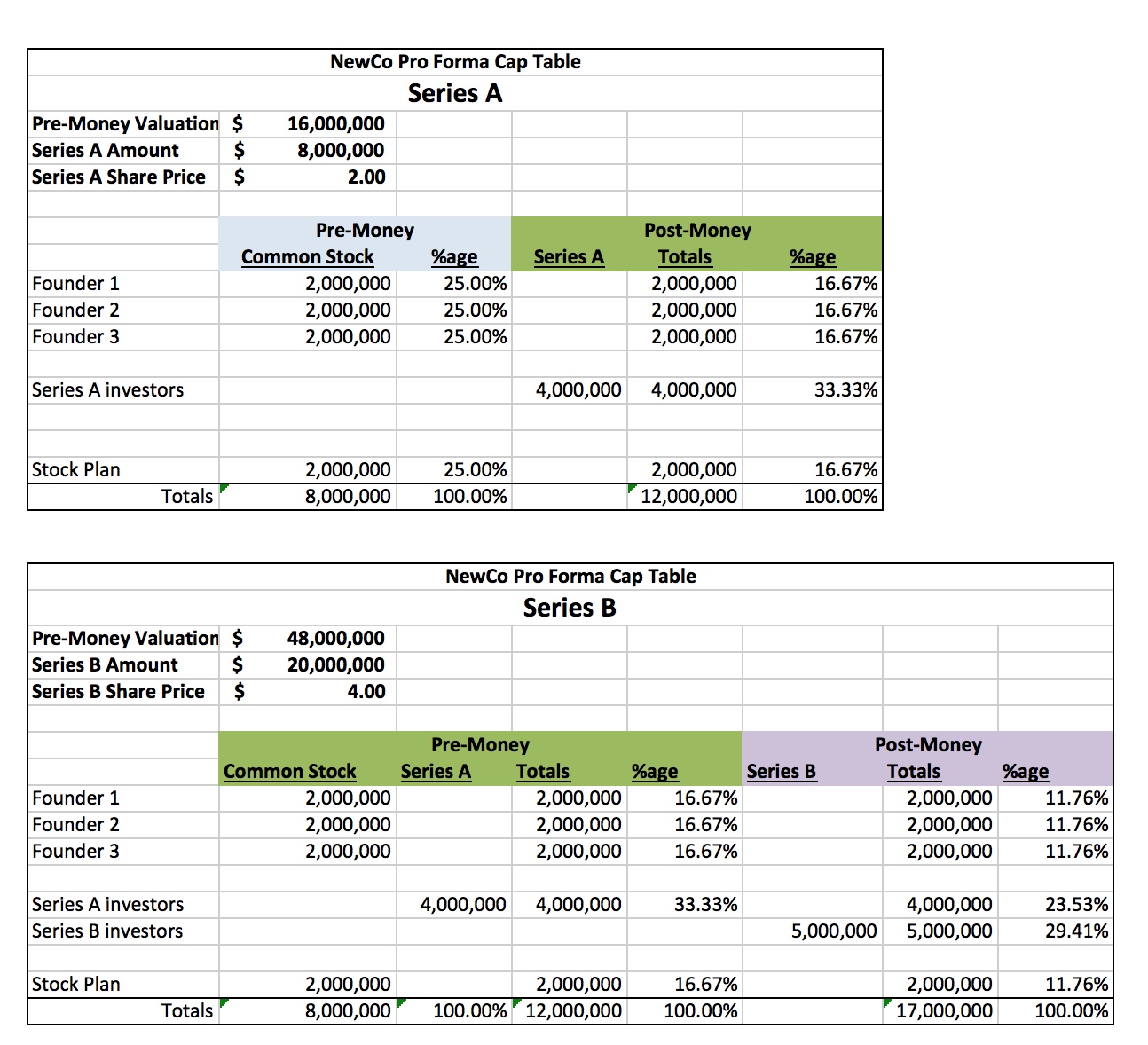

When a company issues new shares at a lower price per share than a prior round, existing investors who paid the higher price suffer two forms of harm: their ownership percentage decreases (percentage dilution), and the implied value of their shares declines (economic dilution).1 The price per share (PPS) formula is PPS = pre-money valuation / fully-diluted shares outstanding. If a company was worth $12M post-Series A (with 12M fully diluted shares at $1.00/share) and then raises a Series B at a $10M pre-money valuation across 12M shares, the new PPS drops to $0.83 — meaning every Series A preferred share now converts to common worth $0.83 rather than $1.00.1

Without any anti-dilution provision, that Series A investor's 3M preferred shares would convert to 3M common shares each worth $0.83, reducing the value of their stake from $3M to $2.5M — a $500K loss solely from the down round, not from any operational deterioration.1 Anti-dilution provisions address this by adjusting the conversion price downward, granting the earlier investor more common shares upon conversion to partially restore the value of their stake.3

The mechanism works by modifying the conversion ratio between preferred and common stock. Preferred stock initially converts 1:1 into common stock. After a down round triggers anti-dilution protection, the conversion ratio becomes greater than 1:1 — meaning each preferred share converts to more than one common share.3 This change affects voting rights (since votes are typically tied to common stock equivalents), the founder's dilution in any subsequent conversion event, and exit proceeds if investors choose to convert.

Full Ratchet Anti-Dilution

Full ratchet anti-dilution is the most aggressive protection available to investors. It resets the conversion price of the protected preferred stock to the lowest price of any subsequent share issuance, regardless of the size of that down round.6 The formula is straightforward: new shares upon conversion = (number of preferred shares) × (original share price / new down-round price).

Using the example above: a Series A investor with 3M preferred shares originally purchased at $1.00/share, facing a down round at $0.83/share, would convert to 3M × ($1.00 / $0.83) = approximately 3.6M common shares under full ratchet.1 This restores the dollar value of the investment but leaves the investor with a larger ownership stake than they originally had, directly diluting founders and employees holding common stock.

Full ratchet provisions are rare in U.S. venture deals because they can be catastrophic to founders in even a modest down round. If a company sells a small bridge round at a discounted price, full ratchet resets every prior investor's conversion price to that bridge price — potentially wiping out founders' equity entirely.4 DLA Piper advises founders to scrutinize full ratchet terms carefully before agreeing to them, noting that future investors may also be deterred by the common-stock dilution that full ratchet creates for any prior round.3

Weighted Average Anti-Dilution

Weighted average anti-dilution is the standard market protection in U.S. venture deals. Instead of resetting the conversion price to the lowest price in any single transaction, it calculates a new conversion price based on the weighted average of all shares outstanding plus shares newly issued.2 The size of the down round matters: a small down round causes a smaller conversion price adjustment than a large one at the same per-share price.5

The weighted average formula is: New conversion price = Old conversion price × (A + B) / (A + C), where A = shares outstanding before the new issue, B = shares that would have been issued at the old price for the same total proceeds, and C = shares actually issued at the new lower price.1 Applying this to the previous example: New conversion price = $1.00 × (12M + $10M/$1.00) / (12M + 12M) = $1.00 × 22M / 24M = $0.917. The Series A investor's 3M shares now convert to 3M / $0.917 = approximately 3.27M common shares — significantly fewer than the 3.6M under full ratchet.1

The formula has two variants based on how "outstanding shares" is defined. Broad-based weighted average includes all issued shares, outstanding options, warrants, and securities convertible to common stock in the denominator.2 Narrow-based weighted average includes only outstanding preferred shares, excluding the option pool and other convertibles. Because the broad-based formula has a larger denominator, it produces a higher (less investor-favorable) new conversion price and grants fewer bonus shares to the anti-diluted investor — making it better for founders and employees while still providing meaningful protection to investors.1 Cooley GO identifies broad-based weighted average as the standard; seeing anything other than broad-based should prompt a conversation with counsel.4

Key Exceptions and Carve-Outs

Anti-dilution provisions typically include a list of excluded issuances that do not trigger the anti-dilution mechanism even if shares are issued below the prior round's price.3 Standard carve-outs include: (1) shares issued to employees and consultants under a board-approved equity incentive plan (options are almost universally excluded), (2) shares issued in connection with equipment leases or bank credit lines, (3) shares issued in strategic partnerships or licensing deals approved by the board, and (4) shares issued in connection with an acquisition.3 The option pool carve-out is particularly significant — the size of the reserved option pool determines how many shares can be granted to employees without triggering anti-dilution for existing preferred holders.

Pay-to-play provisions interact directly with anti-dilution protection. Under a pay-to-play clause, an investor who declines to participate pro rata in a down round forfeits their anti-dilution protection and converts to common stock.7 This mechanism aligns existing investor incentives with company survival and is especially useful in bridge financings where inside investors might otherwise free-ride on new investor capital while retaining their protective provisions.

Negotiation Considerations

Anti-dilution provisions aren't typically found in SAFEs or convertible notes, since those instruments don't represent a fixed percentage ownership until conversion — the valuation cap itself functions as an implicit anti-dilution mechanism by fixing the conversion price.3 Founders negotiating preferred stock financings should push for broad-based weighted average over narrow-based, and should never accept full ratchet without explicit legal counsel.4

Future investors sometimes negotiate away prior investors' anti-dilution protections as a condition of investing in a later round. This can create disputes between investor classes and delay or derail financing — particularly when the prior investors' anti-dilution rights would give them an outsized common stock position that crowds out new investor ownership targets.1 Founders who anticipate future rounds should therefore be cautious about granting narrow-based or full ratchet protections to any single investor, as those provisions become negotiating leverage for that investor in every subsequent down round discussion.7